Asset Allocation ETF Guide: Build a Diversified Portfolio

You don’t need dozens of holdings to build a well-diversified portfolio. A small number of asset allocation ETFs can give you exposure to thousands of global securities in a single trade, at a fraction of the cost of a traditional managed portfolio. This guide shows you how to build one from scratch.

Educational disclaimer This article is for educational and informational purposes only and does not constitute financial, investment, or tax advice. The fee comparisons use publicly available data and illustrative scenarios. Consult a registered financial advisor before making any investment decisions.

Introduction

Prior to the launch of asset allocation ETFs in 2018, the do it your-self investors used mixing and matching ETFs when building their own diversified portfolios. Asset allocation funds or portfolio ETFs, first offered via major investment advisory companies, such as Vanguard, iShares, are built to represent a combination of different asset classes such as equities, bonds and cash.

What are Asset Allocation ETFs?

Asset Allocation ETFs represent a unique investment vehicle that combines the traditional exchange-traded funds with the principles of asset allocation. Unlike conventional ETFs that focus on specific asset classes or sectors, Asset Allocation ETFs combines multiple ETFs, primarily focusing on different asset classes like stocks and bonds, to provide a comprehensive, diversified investment solution within a single fund.

ETFs are comprised of same asset class, for example either stocks or bonds, so they are already diversified within asset classes or sector, while asset allocation ETF combines multiple ETFs to further diversify across asset classes, sectors or geographies. For example, SPDR S&P 500 ETF (SPY) includes stocks from the 500 large-cap US companies, which means it’s diversified within the U.S. large-cap stock market but doesn’t include other asset classes like bonds, or assets stocks/bonds from outside US.

Asset Allocation ETFs may combine SPDR S&P 500 ETF (SPY) with ETF fund comprised of US diversified bonds, e.g., iShares Core U.S. Aggregate Bond ETF (AGG) to further diversify the portfolio across asset classes, stocks and bonds. Now this portfolio of stock and bond ETFs is diversified across the two asset classes, but it is not yet diversified geographically, so we may need to choose a third ETF comprising of stocks of international companies.

Understanding Portfolio Construction with ETFs

Portfolio construction with Asset Allocation ETFs involves a strategic approach to selecting a mix of funds that align with an investor’s unique financial objectives, risk tolerance, and time horizon. Instead of allocating capital to individual stocks or bonds, investors can harness the power of diversification by gaining exposure to multiple asset classes, sectors and foreign markets through a professionally selected and managed ETFs.

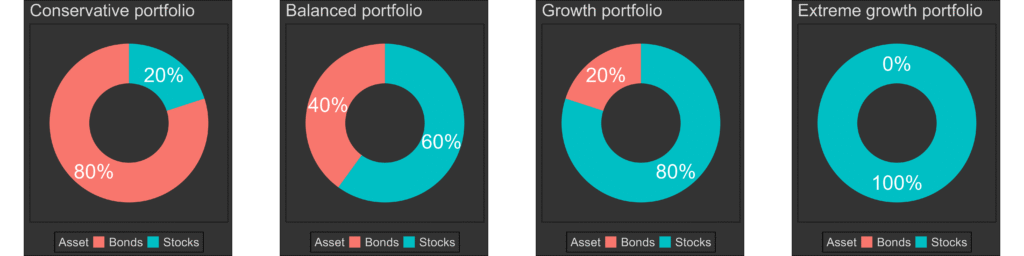

The stocks (i.e. equity class) portion gives more growth power over time but makes the portfolio more susceptible to significant losses. The bonds (i.e., fixed income asset class) do not give much power to grow but it reduces the risks and introduces stability, so the portfolio is less likely to incur significant losses. Combining the two different asses classes (equities and bonds) takes the best of the both worlds, it enables balance between the power to grow while having some level of stability. The (donut) charts above illustrate four different allocations for stocks and bonds and their respective risk level (Conservative, Balanced, Growth, Extreme growth).

If interested, the Canadian portfolio case study example is here.

Are asset allocation funds good?

Pros:

The last but not least advantage of ETF portfolios is its cost-effectiveness. Compared to actively managed portfolio or constructing a traditional portfolio of individual securities, ETF portfolios typically have lower costs. By minimizing the expenses, investors can potentially maximize their returns over the long term.

The primary advantage of Asset Allocation ETF portfolios is diversification. By investing in diversified ETF portfolios, investors spread their risk across multiple asset classes and minimize the exposure to any single sector or geographical market. This in turn helps reduce the impact of market volatility in the long run.

The secondary advantage of Asset Allocation ETF portfolios lies in the simplicity of the investment strategy. Unlike traditional portfolio construction based on individual stocks, bonds and cash, the all-ETF portfolios provide investors with diversified access to various asset classes, from different sectors and geographical regions. All this is done via a single fund managed by professional financial managers. Hence, you do not need to be an investment expert to benefit from long-term investing in all-ETF diversified portfolios. In fact, the investment literature shows that on the long run, investing in diversified funds can be a good strategy to build wealth for personal DIY investors.

The third, like the traditional portfolios, all-ETF portfolios can be built to adapt to investor investment goals, risk tolerance and time horizon.

Cons:

- Not available via brick and mortar banks, these are available via online brokerage accounts.

- It may add up brokerage imposed transactional and loading costs.

- Complexity of managing ETFs can increase, especially when dealing with large numbers of ETFs and their respective allocations.

- Tax implications, although ETFs are tax efficient, taxes can incur for investments held in taxable accounts.

- Managing an all-ETF portfolio can become complex, especially when dealing with a large number of ETFs to achieve desired diversification. This complexity might be overwhelming for less experienced investors.

Why is asset allocation good?

Similarly to the traditional portfolio, asset allocation’s primary role is to maintain stability of the investment over the investment horizon while balancing the appetite for the portfolio returns with risks at acceptable levels.

ETF portfolios are constructed to maintain a target allocation to each asset class, sector or geographical region, having the underlying ETFs periodically rebalanced to ensure the desired target allocations are preserved. Deviations from the target allocations may affect the originally projected returns and risks. This systematic approach to portfolio management ensures that investors can adapt to ever-changing market conditions and ultimately maintain their investment objectives.

For example, a growth asset allocation portfolio may be comprised of ETFs that follow indices of stocks, bonds and cash, with specific higher percentage allocated to the stock assets, smaller percentage allocated to bonds, and miniature percentages allocated to cash. Over time the asset allocation percentages my change, stock portion of the portfolio may grow larger than the target allocation for stocks, reducing the allocated percentages for the bonds and this needs rebalancing. Managers utilize different strategies to portfolio rebalancing, such as buying an holding more of the other asset classes until the original target percentage allocations are restored.

What is a good asset allocation by age?

Asset allocation by age usually pertains to the time when the investor plans to start withdrawing money from the portfolio (e.g., retirement). In retirement portfolios, (for example Vanguard’s target day portfolios) the earlier in the investment horizon, the allocation weight is heavier on the equities part and lower on the bonds part, which allows portfolio growth at increased risk. As the retirement date approaches, the allocation shifts towards fixed income assets such as bonds, to stabilize the risks prepare for fund withdrawals.

For example, during a market downturn it would not be ideal to withdraw funds from the portfolio, as this would mean selling stocks at lower prices, so the investor would have to wait for the market to recover in order to sell stocks and withdraw liquid cash. However, if there is sufficient bond allocation in the portfolio during the market downturn, the investor may receive income from the bonds, providing a more stable source of income.

What is a good portfolio allocation?

As with traditional portfolio, a good portfolio allocation with depend on investor risk tolerance, time horizon and investment goals. In this section, we’ll explore four common asset allocation strategies:

- Aggressive Growth Allocation

- Conservative allocation

- Balanced Allocation

- Growth Allocation

Conservative Allocation

Conservative allocation typically includes a higher proportion of bonds and a smaller proportion of equities to minimize risk. Allocation Example: 60% Bonds (e.g., bond ETFs), 40% Equities (e.g., equity ETFs). Conservative allocation tends to keep the portfolio value stable even when the stock market experiences fluctuations. The conservative allocation is typically recommended in the last few years before the end of the investment time horizon (e.g., retirement). For example, at the beginning of the investment years, the goal is to grow the portfolio while maintaining the risk at acceptable levels, but after the portfolio has accomplished it’s goal and it is approaching the time for withdrawals, the portfolio allocations are typically transitioning into conservative allocation to avoid having to deal with withdrawals at the time when the stock market takes a downturn.

For example, the Vanguard Conservative ETF Portfolio (VCNS), as the name suggest, has the following allocation: Stocks 40.59%, bonds 59.36% and short-term reserves 0.05%.

Data Source: Yahoo Finance Data, plots generated with R package quantmod, tidyverse and knitr

Vanguard Conservative ETF Portfolio Fund allocation

Vanguard Conservative ETF Portfolio (VCNS) Fund allocation

Fund

Allocation

Vanguard Canadian Aggregate Bond Index ETF

34.94%

Vanguard U.S. Total Market Index ETF

17.96%

Vanguard Global ex-U.S. Aggregate Bond Index ETF (CAD-hedged)

12.61%

Vanguard FTSE Canada All Cap Index ETF

12.23%

Vanguard U.S. Aggregate Bond Index ETF (CAD-hedged)

11.82%

Vanguard FTSE Developed All Cap ex North America Index ETF

7.47%

Vanguard FTSE Emerging Markets All Cap Index ETF

2.93%

Balanced Allocation

Balanced allocation typically includes approximately similar proportion to stocks and bonds. Allocation Example: 40% Bonds (e.g., bond ETFs), 60% Equities (e.g., equity ETFs). Compared to conservative allocation, balanced allocation comes with the power of stable growth over time.

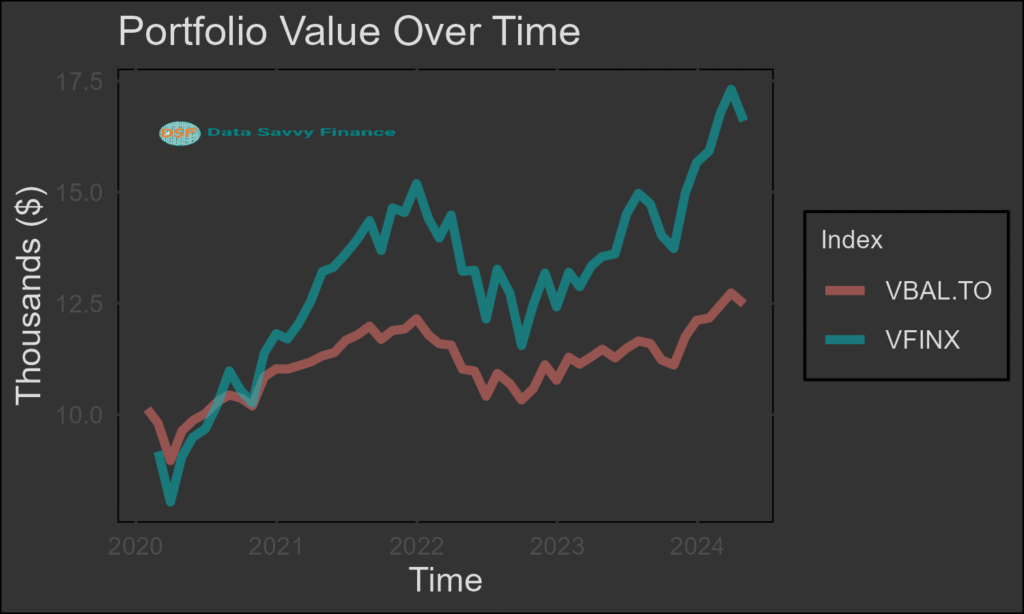

For example, the Vanguard Balanced ETF Portfolio (VBAL), as the name suggest, has the following allocation: Stocks 60.57%, bonds 39.38% and short-term reserves 0.05%.

Investment Portfolio

Vanguard Balanced ETF Portfolio (VBAL)

Fund

Allocation

Vanguard U.S. Total Market Index ETF

26.92%

Vanguard Canadian Aggregate Bond Index ETF

23.32%

Vanguard FTSE Canada All Cap Index ETF

18.11%

Vanguard FTSE Developed All Cap ex North America Index ETF

11.21%

Vanguard Global ex-U.S. Aggregate Bond Index ETF (CAD-hedged)

8.30%

Vanguard U.S. Aggregate Bond Index ETF (CAD-hedged)

7.77%

Vanguard FTSE Emerging Markets All Cap Index ETF

4.32%

Growth Allocation

Growth allocation typically includes large proportion of stocks and a small proportion of bonds. Allocation Example: 20% Bonds (e.g., bond ETFs), 80% Equities (e.g., equity ETFs). The growth allocation, enables the portfolio to grow higher while also having some stability over time. As the name suggests, this portfolio could be used while the portfolio is in the growth stage, for example a couple of decades before retirement.

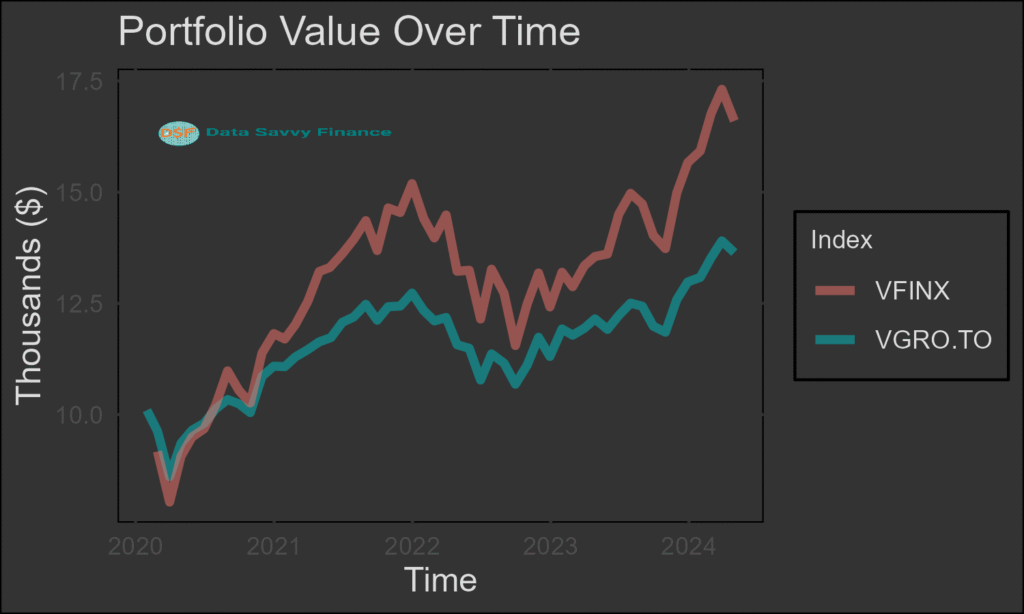

For example, the Vanguard Growth ETF Portfolio (VGRO), has the following allocation: Stocks 80.59%, bonds 19.37% and short-term reserves 0.04%.

Investment Portfolio

Vanguard Growth ETF Portfolio (VGRO)

Fund

Allocation

Vanguard U.S. Total Market Index ETF

36.19%

Vanguard FTSE Canada All Cap Index ETF

23.63%

Vanguard FTSE Developed All Cap ex North America Index ETF

15.30%

Vanguard Canadian Aggregate Bond Index ETF

11.64%

Vanguard FTSE Emerging Markets All Cap Index ETF

5.47%

Vanguard Global ex-U.S. Aggregate Bond Index ETF (CAD-hedged)

3.99%

Vanguard U.S. Aggregate Bond Index ETF (CAD-hedged)

3.74%

Aggressive Growth Allocation

Aggressive growth allocation typically includes large proportion of stocks and no bonds. Allocation Example: 0% Bonds (e.g., bond ETFs), 100% Equities (e.g., equity ETFs). The aggressive growth allocation, enables the portfolio to grow higher. As the name suggests, this portfolio allocation could be used while the portfolio is in the growth stage, for example a couple of decades before retirement.

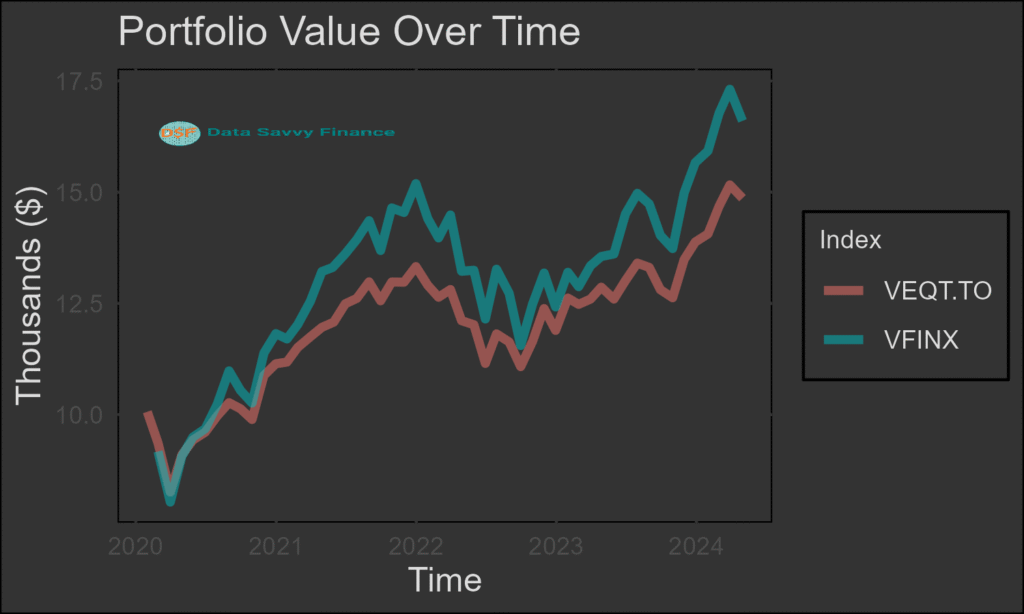

For example, the Vanguard All-Equity ETF Portfolio (VEQT), has the following allocation: Stocks 99.96%, bonds 0.00% and short-term reserves 0.04%.

Vanguard All-Equity ETF Portfolio (VEQT)

Vanguard All-Equity ETF Portfolio (VEQT)

Fund

Allocation

Vanguard U.S. Total Market Index ETF

44.95%

Vanguard FTSE Canada All Cap Index ETF

29.55%

Vanguard FTSE Developed All Cap ex North America Index ETF

18.63%

Vanguard FTSE Emerging Markets All Cap Index ETF

6.83%

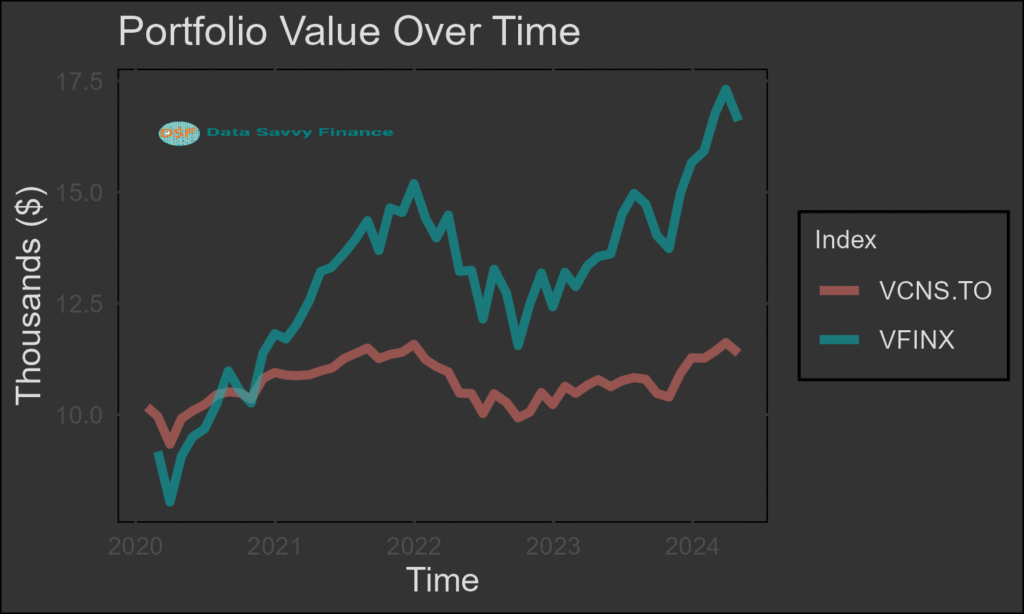

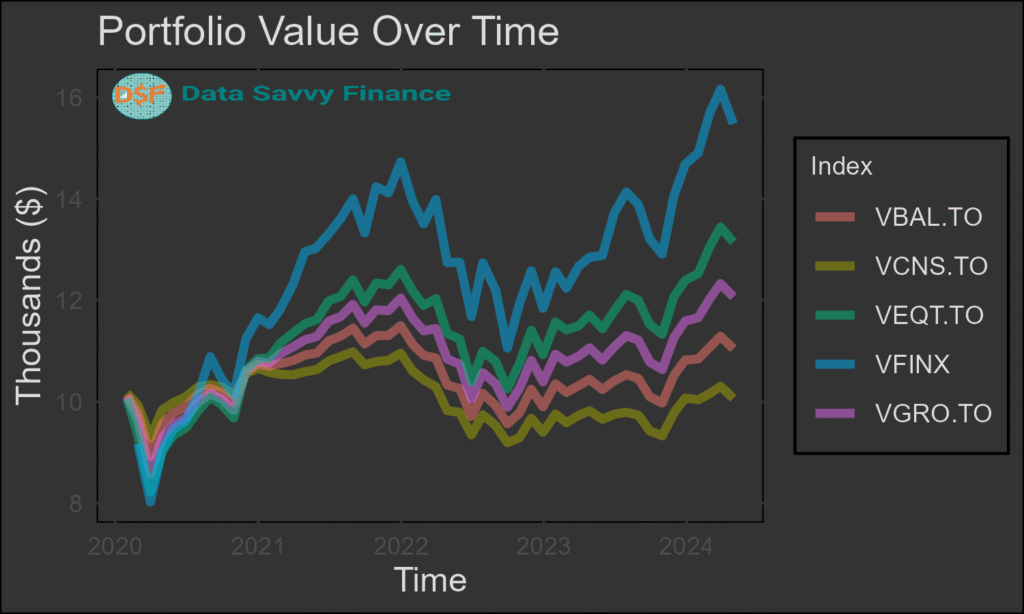

Initial investment of 10,000 on January 1st 2020 would achieve a balance of $14,863 on April 30, 2024, marking an Compound Annualized Growth Rate (CAGR) of 9.58%, as shown in the graph. Compared to a benchmark index fund Vanguard 500 Index Investor (VFINX), which tracks market-cap-weighted portfolios of 500 largest US stocks, the VEQT offers much larger growth than the VCNS, VBAL or VGRO, at the expense of increased risk, as measured by annualized standard deviation of 14.47%. In contrast, VFINX exhibited dramatic growth up to $16,601 marking a CAGR of 12.68%, followed by larger downfall in the 2022 post-pandemic period, exhibiting a much higher risk as measured by annual standard deviation of 19.43%. The risk-adjusted CAGR for VGRO and VFINX are 8.19% and 10.22%, respectively.

Why is the VEQT annualized return and the risk lower than that of VFINX, when they are both based on equities only?

The VEQT fund allocation table above indicates that VEQT comprises geographically diversified ETF stock funds, comprising not only the US total stock index (Vanguard U.S. Total Market Index ETF), but also the Canadian total stock index (Vanguard FTSE Canada All Cap Index ETF), developed except North American stocks (Vanguard FTSE Developed All Cap ex North America Index ETF) and emerging total stock (Vanguard FTSE Emerging Markets All Cap Index ETF) indices. This geographical diversification is the main contributing factor that drives lower risk for the VEQT compared to that of the VFINX, but also reduces the potential growth on the returns.

The VEQT fund allocation table above indicates that VEQT comprises geographically diversified ETF stock funds, comprising not only the US total stock index (Vanguard U.S. Total Market Index ETF), but also the Canadian total stock index (Vanguard FTSE Canada All Cap Index ETF), developed except North American stocks (Vanguard FTSE Developed All Cap ex North America Index ETF) and emerging total stock (Vanguard FTSE Emerging Markets All Cap Index ETF) indices. This geographical diversification is the main contributing factor that drives lower risk for the VEQT compared to that of the VFINX, but also reduces the potential growth on the returns.

Portfolio Performance

Metric

VCNS.TO

VBAL.TO

VGRO.TO

VEQT.TO

VFINX

Start balance

10000.00

10000.00

10000.00

10000.00

10000.00

End balance

11380.23

12485.43

13640.83

14863.55

16601.50

AnnualizedReturn

(CAGR)

3.03

5.26

7.43

9.58

12.68

St.Dev Monthly

2.52

3.03

3.60

4.18

5.61

St.Dev annually

8.72

10.50

12.48

14.47

19.43

Risk adjusted CAGR

2.76

4.73

6.54

8.24

10.27

Conclusion

Asset Allocation ETF portfolios offer investors a convenient, cost-effective, and efficient way to build diversified investment portfolios tailored to their financial goals and risk tolerance.

Stay tuned for Post 2: Types of Asset Allocation ETF Portfolios!